The Industry of Confusion

The financial industry is designed to be confusing. It invents words like “quantitative easing” and “derivatives” to make you feel stupid. If you feel stupid, you hire a manager. If you hire a manager, they get paid fees. It is a business model built on insecurity.

But after twenty-five years of watching markets, I can tell you a secret. The principles that actually work fit on a single index card. Everything else is just sales. Wealth isn’t built by finding a secret algorithm. It is built by doing simple things for a long time. It is about behavior, not math. Here are the key principles that separate the wealthy from the worried.

The Gap is everything.

There is only one number that matters in personal finance. It isn’t your salary. It isn’t your investment return. So, it isn’t your credit score. Yes, it is The Gap. The Gap is the difference between what you earn and what you spend.

If you earn $500,000 and spend $500,000, your gap is zero. You are broke. You are just a high-income, broke person. If you earn $50,000 and spend $40,000, your gap is $10,000. You are building wealth.

Most people focus entirely on the income side of the equation. They hustle for raises. So they switch jobs. They start side hustles.

But if they don’t fix the spending side, the gap never widens. This is called “lifestyle creep.” The moment you get a raise, you buy a nicer car. You move to a better apartment. And start buying the $60 wine instead of the $15 wine. You feel richer, but your balance sheet is flat.

The first principle of wealth is to defend the gap. When income goes up, expenses should stay flat. That is how freedom is bought.

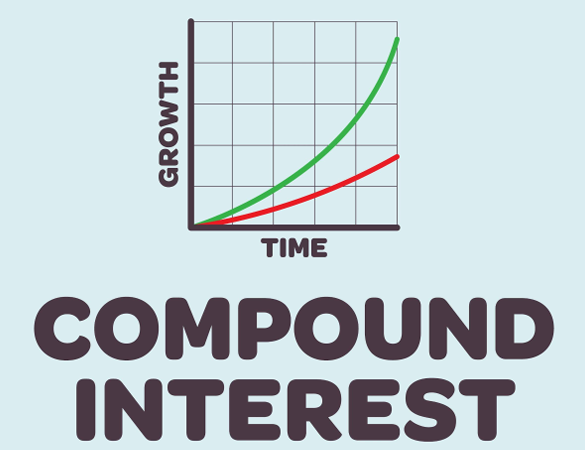

Compound Interest is the Eighth Wonder

Albert Einstein (allegedly) called compound interest the eighth wonder of the world. “He who understands it earns it; he who doesn’t pays it.” Humans are bad at understanding exponential growth. We think linearly. If I take 30 steps linearly, I walk across the room. If I take 30 steps exponentially (1, 2, 4, 8, 16…), I walk around the earth 26 times. Money works exponentially.

The first $100,000 is the hardest. It takes years of grinding. It feels like pushing a boulder up a hill. But once you have that capital working, the math changes. The interest starts earning interest. The principle here is simple: start early. A mediocre investor who starts at 22 will crush a genius investor who starts at 40. Time is the heaviest weight on the scale. Waiting for the “perfect time” to invest is the most expensive mistake you can make. The perfect time was yesterday. The second best time is today.

Debt is a Double-Edged Sword

Debt is not inherently evil. It is a tool. But it is a tool like a chainsaw. It can build a house, or it can cut off your leg. It depends on how you hold it. There are two types of debt. This is debt used to buy things that lose value. Credit card debt for clothes. Auto loans for luxury cars. This debt compounds against you. It is the reverse of Principle #2. You are paying interest on something that is worth less every day. This is financial suicide.

Productive Debt:

This is debt used to buy assets that gain value. A mortgage on a rental property. A loan to start a profitable business. This debt can accelerate wealth if the asset produces enough cash flow to service it.

the debt. The principle? Never use debt to fund a lifestyle. Only use it to fund an asset. If you cannot pay cash for the vacation, you cannot afford the vacation. That is a hard rule. But it keeps you safe.

Liquidity is oxygen.

Net worth is vanity. Liquidity is sanity. You can be “rich” on paper and go bankrupt on Tuesday.

I have seen real estate developers with $50 million in assets lose everything. Because they couldn’t pay a $10,000 tax bill on time. Their wealth was illiquid. It was trapped in dirt and concrete. You need a liquidity buffer.

This is commonly called an emergency fund. I prefer calling it a “Freedom Fund.” It is 3-6 months of expenses sitting in boring, safe cash. It earns nothing. Inflation eats it a little bit every year. That is okay.

The “return” on this cash isn’t interest. The return is sleep.

So, a return is an option. When you have liquidity, you don’t have to sell your stocks when the market

crashes just to buy groceries. You don’t have to take the first job offer out of desperation. Liquidity buys you the ability to say “No.” That is the ultimate luxury.

Automation Beats Willpower

You are not as disciplined as you think you are. Willpower is a muscle. It gets tired. By Friday afternoon, after a long week of work, your willpower is gone. You will buy the pizza. And will skip the gym. You will not transfer money to your savings account. The principle is to remove the human element. Check automation in finance.

Automate everything.

Set up your 401(k) to deduct from your paycheck before it hits your bank account. You cannot spend what you do not see. Set up auto-pay for your credit cards. Set up auto-transfer for your investment

accounts. The goal is to make good decisions the default and bad decisions difficult. If you have to log in and manually transfer money to save, you will fail.

If you have to log in and manually transfer money to spend it, you will save. Build a system that works even when you are lazy. Because you will be lazy sometimes.

Risk Capacity vs. Risk Tolerance

These two sound the same. They are opposites. Risk tolerance is how you feel about losing money. It is emotional. Everyone thinks they have high tolerance until the market drops 20%. Then they panic.

Risk capacity is how much money you can afford to lose without ruining your life. It is mathematical.

A 25-year-old with no kids and a stable job has high risk capacity. If the market crashes, they have 40 years to recover.

A 65-year-old retiree living off their portfolio has low risk capacity. If the market crashes, they might not be able to pay for heat. The principle: Your capacity must dictate your tolerance. Don’t invest aggressively just because you “feel lucky.” Invest based on your timeline and your needs.

If you need the money in 3 years for a down payment, it does not belong in the stock market. The market is a casino in the short term. It is a wealth-building machine in the long term. Match the asset to the timeline.

The Invisible Tax of Fees

In 2026, many people think investing is free. It isn’t. Fees are the silent killer of portfolios. A 1% fee sounds small. It sounds fair. But do the math. If the market returns 7% and you pay 1% in fees, you aren’t losing

1% of your money. You are losing 14% of your profit.

Over 30 years, a 1% fee will consume about one-quarter of your total potential wealth. Wall Street loves high fees. They hide them in “Expense Ratios” and “Assets Under Management” costs. The principle is to control what you can control. You cannot control the market return. You can control the cost. Stick to low-cost index funds. Avoid expensive active managers who promise to beat the market. (Spoiler: They usually don’t).

Diversification is the Only Free Lunch

There is only one free lunch in finance. It is diversification. Usually, to get higher returns, you must take higher risks. But if you combine assets that move differently (stocks, bonds, real estate, and international), you can actually lower your risk without lowering your expected return.

If you own one stock, you have a “single point of failure” risk. And if the CEO tweets something crazy, you lose 20%. If you own the S&P 500, you own 500 companies. One crazy CEO doesn’t matter. Don’t look for the needle in the haystack. Just buy the haystack.

Behavior is the Enemy

The biggest threat to your financial future isn’t the economy. It isn’t the president. It isn’t inflation.

Yes, it is the person looking back at you in the mirror. We are hardwired to be bad at investing. Our brains evolved on the savannah. When we saw a threat (a lion), we ran. When we saw a reward (food), we grabbed it. In the market, this instinct is fatal. When the market crashes (threat), our brain screams, “Sell!” This locks in losses. When the market soars (reward), our brain screams, “Buy!” This means we buy at the top. The principle: Invert your instincts.

When the headlines are terrifying, that is usually the best time to buy. When your cab driver is giving you stock tips, that is usually the time to worry. Successful investing is mostly about impulse control. It is about doing nothing when everyone else is freaking out.

Start Today

This is the final and most important principle. Analysis Paralysis is real. People read blogs (like this one). They listen to podcasts. They research the perfect ETF. And they do nothing. They wait for the “right moment.” There is no right moment. The market is always scary. There is always a war, a recession, or an election looming.

If you waited for a calm year to invest, you would have never invested. The cost of waiting is astronomical. If you invest $500 a month starting at 25, you have over $1 million at 65.

If you wait until 35 to start, you have half that amount. Ten years of delay costs you $500,000. Don’t wait to be an expert. You don’t need to know everything. Open the account. Buy the index fund. Set up the auto-transfer. Then go live your life.

Summary

Wealth is simple.

Spend less than you earn. Invest the surplus. Avoid debt. Stay diversified. Don’t panic. If you do those five things, you will win. This won’t happen overnight. It will be boring. It will be slow. But it will be inevitable.

Disclaimer

Look, Admin has been doing this a long time, but I’m a strategist, not your specific financial advisor or lawyer. The markets and regulations mentioned here, like the FinCEN rules or tariff situations, change faster than the weather. This article is meant to make you think strategically, not to replace professional advice tailored to your exact situation. Always do your own due diligence and consult with qualified professionals before making major moves.