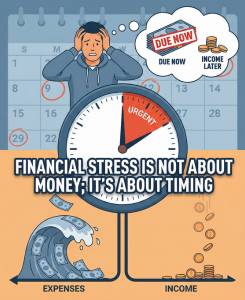

The Solvency Illusion

Seven years of analyzing market failures reveals a specific, recurring truth. Companies rarely go bankrupt because they lack assets. They go bankrupt. because they cannot pay a bill on a Tuesday, even if a massive check is clearing on Thursday. There is a widespread belief that the cure for financial anxiety is a higher salary. This is the “Solvency Illusion.” It suggests that if the total income column is larger than the total expense column, stress should vanish. It does not.

A person earning $150,000 a year can experience the exact same visceral panic as someone earning $50,000. The math says they are rich. The calendar says they are broke. Financial stress is rarely a function of volume. It is a function of flow. It is a timing problem masquerading as a poverty problem.

The Gap Between the Ledger and Life

Accountants look at money in 30-day buckets. Life happens in 24-hour increments. The spreadsheet says there is a surplus of $500 at the end of the month. The spreadsheet is technically correct. But the spreadsheet doesn’t know that the rent is due on the 1st, and the paycheck doesn’t hit until the fifth.

That four-day gap is where the misery lives. During those 96 hours, you are technically solvent but effectively bankrupt. You are borrowing from peace of mind to pay for a calendar error.

We need to stop looking at “Net Worth” and start looking at “Net Timing.” When bills arrive before salary and rumors about new taxes spread, people don’t calculate. They panic.

Framework 1: Delay Damage

In strategy, speed is a currency. In personal finance, the opposite is true. Delay is a cost. I call this “Delay Damage.” It isn’t just the late fee. That is the visible cost. That is easy to calculate. $35. Fine. The real damage is the secondary effect. When money is tight because of timing, you delay maintenance. You hear a noise in the car engine. You know it needs a mechanic. But the paycheck is three days away. So you wait.

In those three days, the small noise becomes a catastrophic failure. The $200 repair becomes a $2,000 engine replacement.

That is delayed damage.

It happens in health too. You delay the dentist. You delay the checkup. The problem compounds. Poor timing forces you to make decisions that are expensive in the long run but necessary in the short run. It forces you to buy the smaller, more expensive pack of toilet paper because you can’t afford the bulk pack today. You are paying a premium for being out of sync.

The Panic of the 1st and 15th

Most of the world runs on a rigid rhythm. Mortgage on the 1st. Utilities on the 15th. If your income stream is irregular—freelance, commission, or just biweekly on the wrong weeks—you are fighting gravity.

The stress comes from the misalignment.

I see high-net-worth individuals sweating over a credit card bill. Why? Because their wealth is illiquid. It is locked in a house or a retirement account. You cannot buy groceries with a 401(k) balance. They have money. They just don’t have it now.

Framework 2: Expense Elasticity

Not all bills are created equal. Some bend. Some break. This concept is “expense elasticity.” A grocery bill is elastic. You can buy steak, or you can buy rice. You can spend $300, or you can spend $50. So, you control the timing and the magnitude. A mortgage is inelastic. It is $3,200.

This is due on the 1st. It does not care if you had a bad week. It does not care if your client paid late. Financial stress usually spikes when an inelastic expense hits a liquidity gap. When you have flexible expenses, you feel in control. You can maneuver. When you have rigid expenses, you feel trapped. The goal of financial management isn’t just to lower expenses. It is to increase elasticity.

It is better to have a $500 variable cost than a $400 fixed cost. The fixed cost kills you on the bad months. The variable cost breathes with you.

The “Float” Trap

Credit cards were invented to solve this timing problem. They provide a 30-day “float.” But for many, the solution became the poison. They use the card to bridge the gap between the 1st and the 5th. Then the next month, the gap widens. The bridge becomes a crutch. Suddenly, you are paying interest on your groceries from three months ago. The timing problem has metastasized into a debt problem.

It started innocently. You just needed to sync the cash flow. But because the underlying rhythm was never fixed, the debt cycle became permanent.

Framework 3: Emotional Tax Load

There is a psychological weight to juggling. I call this the “Emotional Tax Load.” Every time you have to check your bank balance before buying a coffee, you pay a tax. Not a money tax. A mental tax. It consumes bandwidth. If you have to log in to three different apps to see if a check cleared so you can pay the electric bill, you are burning cognitive energy that could be used for your career.

People with bad timing work harder than people with good timing. They are constantly managing the logistics of scarcity. They are moving money from savings to checking, then back again. So, they are calling vendors to ask for extensions. This is exhausting.

It explains why people make bad decisions when they are broke. This isn’t because they are stupid. It is because their brain is tired. The emotional tax load has depleted their decision-making reserves.

The Anatomy of a Bad Week

Let’s walk through a typical scenario. It is Tuesday. The rent check was mailed on Monday. The paycheck is direct deposited on Friday. The car blows a tire. If the timing were aligned, this would be an annoyance. You swipe the card, and you fix the tire.

But because the rent check is floating in the ether, you don’t know the “real” balance. The bank says you have $2,000. But $1,800 is spoken for. So you hesitate. You drive on the spare tire. You risk an accident. That stress about it all day at work. Your productivity drops. Your boss notices.

The stress isn’t about the $150 for the tire. It is about the uncertainty of the window. It is about the fear of the overdraft fee. The fear of the bounced check notification. That fear is corrosive. It eats relationships. Spouses fight about money usually because the timing didn’t line up, not because they are starving.

- “Why did you buy that today?”

- “Because we needed it.”

- “But the auto-pay hits tomorrow!”

- That is a timing argument

The Liquidity Buffer Solution

So, how do you fix this without winning the lottery? You stop trying to time the market of your own life.

You need to decouple your income from your expenses. The goal is to get one month ahead. Just one.

If you earn $5,000 a month, you need $5,000 in the checking account before the month starts.

If you want to study more exactly what a liquidity buffer is, check this liquidity buffer. This sounds impossible. “If I had $5,000 extra, I wouldn’t be stressed.” But you don’t need it all at once. You build it slowly. You tackle “Delay Damage” first. Fix the things that are leaking money.

Then you attack “Expense Elasticity.” You negotiate the rigid bills. You try to move due dates. Did you know you can call utility companies and ask to change your billing date from the 1st to the 15th? Most people never ask. If you move the heavy, inelastic bills to the days after you get paid, you instantly

reduce the timing risk. You align the outflow with the inflow.

The Myth of the “Number”

We are obsessed with “The Number.” How much do I need to retire? How much do I need to be happy? The number is irrelevant if the timing is wrong. You can have a million dollars in real estate and be unable to buy lunch. You can have a million dollars in a 401(k) and lose your house because you missed three mortgage payments.

Liquidity is the oxygen of finance. Net worth is just the muscle. You can be huge and muscular, but if you don’t have oxygen, you die in three minutes. Financial peace comes from liquidity. It comes from knowing that the bill due on Tuesday is covered by the money that arrived last month, not the money arriving

next week.

Breaking the Cycle

The shift from “Timing Stress” to “Timing Peace” is quiet. It happens when you stop checking the banking app every morning. It happens when a bill arrives in the mail, and you don’t feel a spike of adrenaline. You just open it. You pay it. So you throw it away

You haven’t necessarily earned more money. So, you have just mastered the flow. You have eliminated the emotional tax load. So you have repaired the delay damage. They are no longer fighting the calendar.

The Executive Summary of Your Life

If you ran your household like a business, you would fire the CFO if they managed cash flow this poorly. Businesses use “Lines of Credit” to smooth out timing bumps. Individuals use credit cards. The mechanism is the same, but the discipline is usually missing. You need to become the strategist of your own timeline. Look at your month. Where are the choke points? Where does the red line get too close to the black line?

That is your stress point. Don’t focus on saving $3 on coffee. Focus on moving that $2,000 mortgage

payment to a day where it doesn’t hurt. Focus on building a “timing buffer” of $1,000 that sits in the account and never moves. It is just there to absorb the shocks.

The Final Reality

Money is a tool. Time is the context in which we use it. If you use the tool at the wrong time, you break the project. We teach our kids to save. But we teach them to invest.

We rarely teach them that $100 on Monday is worth more than $100 on Friday if the bill is due on Wednesday. That knowledge gap is where the anxiety breeds. Fix the timing. The money will follow.

We rarely teach them to schedule.

Disclaimer

This article is for financial awareness and money management education only. It does not provide investment, legal, or tax advice, and does not

recommend any financial products. ADMIN is not responsible for any uncertain condition if you invest on any platform because we have not advised you to invest