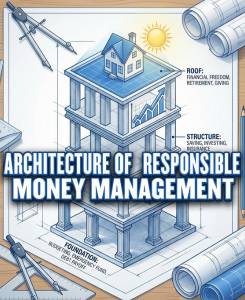

The Roof Without Walls

In twenty-five years of market strategy, I have seen a thousand portfolios. Most of them look like a house built by a child. They have a beautiful, expensive roof. They own Bitcoin. Yes, they own Nvidia. They have aggressive growth ETFs. But they have no walls. And they have no foundation. When the financial weather is sunny (a bull market), the house stands. It looks impressive from the street. The neighbors are jealous.

But when the storm comes—and the storm always comes—the structure collapses. The roof crashes down because there was nothing holding it up. Financial failure is rarely a problem of investment selection. It is almost always a problem of architecture. People try to build wealth in reverse. They obsess over the decoration (stock picking) before they have poured the concrete (cash flow). This is a blueprint for the only house that matters: the one you have to live in when the economy turns cold.

Phase 1: The Concrete Foundation (Liquidity)

No architect starts with the shingles. They start with the dirt. In finance, the dirt is your cash flow. The concrete is your liquidity. Most people hate this phase. It is boring. It is invisible. You cannot brag about

your emergency fund at a dinner party. But without it, you are building on sand.

The Gap

The structural integrity of your financial life depends entirely on one variable: the gap. This is the difference between what flows in and what flows out. If you earn $500,000 and spend $500,000, you have zero structural strength. A single crack—a job loss, a lawsuit, a medical event—brings the whole house down. I have seen high-income earners with zero gap. They are terrified. They live in a mansion made of cards.

The Liquidity Buffer

Concrete takes time to cure. Liquidity takes time to build. You need a “Freedom Fund.” Not an emergency fund. An emergency fund is for fixing a flat tire. A Freedom Fund is for walking away from a toxic job. It is for waiting out a recession without selling your stocks. Three to six months of expenses. In cash. Earning boring interest.

This money is not an investment. It is an insurance policy against your own bad decisions. When you have liquidity, you don’t panic. When you don’t panic, you don’t sell at the bottom. That is the foundation. If you don’t have this, stop reading. Go build it. Do not buy a single stock until the concrete is dry.

Phase 2: The Structural Beams (Risk Management)

Once the foundation is set, you frame the house. You put up the beams that hold the weight. In finance, these beams are insurance and estate planning. I know. You just fell asleep. Wake up. This is where wealth is preserved. You are the primary asset. Your ability to wake up and earn money is the engine of the entire machine. If that engine stops, the house goes dark. Most people are woefully underinsured.

They rely on the cheap policy from HR. That is a mistake. You need “own-occupation” disability insurance. If you are a surgeon and you hurt your hand, you can’t work. A generic policy might say, “You can still be a greeter at Walmart, so we won’t pay you.” An own-occupation policy pays you because you can’t be a surgeon.

The Legal Walls

Then there is the legal structure. If you die without a will, the state decides who gets your house. The state is a terrible architect. But a will is just a piece of paper. You need a trust. A trust is a container. It holds your assets privately. It bypasses the public nightmare of probate court. It creates a wall between your wealth and the world. If you have a net worth and you don’t have a trust, you are driving without a seatbelt. It is fine until it isn’t. Then it is catastrophic.

Phase 3: The Roof (Investments)

Now. Finally. We can talk about the roof. This is the part everyone loves. The stocks. The bonds. The real estate. The purpose of the roof is not to look pretty. It is to protect you from the elements. In finance, the “elements” are inflation and taxation.

If you keep your money in the foundation (cash), inflation eats it. The roof must grow faster than the cost of living. This is why we own equities (stocks). Companies can raise prices. They can adapt. They are a living hedge against a devaluing currency. But a roof made entirely of glass (100% tech stocks) will shatter in a hail storm.

The Asset Allocation

This is the pitch of the roof.

● Stocks are the steep part. They shed water fast, but they are dangerous to walk on.

● Bonds are the flat part. They hold snow, but they are stable. A responsible architect matches the pitch to the climate. If you are 25 (Spring), you can have a steep roof. You have time to recover from a slide.

If you are 65 (Winter), you need a flatter roof. You cannot afford to fall off. The mistake is trying to change the roof every time it rains. I see investors selling stocks because the news is bad. That is like tearing off your shingles because it is raining. That is exactly when you need the roof the most. For more and deeper study, you can check Smart Money Management.

Diversification is Weatherproofing

You don’t build a house out of one material. You use wood, brick, glass, and steel. If you put all your money in one stock, or one sector, you have built a house out of straw. Diversification is the admission that we don’t know the future. We own some things that do well in inflation (real estate). We own some things that do well in deflation (Bonds). We own some things that do well in growth (stocks). We build a structure that can survive any weather, not just the weather we hope for.

Phase 4: The Interior Systems (Tax Efficiency)

A house needs plumbing and electricity. It needs to be efficient. In finance, this is tax planning. It is not about how much you make. It is about how much you keep. This is where you put the furniture. You don’t put a toilet in the living room. And you don’t put a high-yield bond fund in a taxable brokerage account.

Tax-Inefficient Assets (Bonds/REITs): Put them in the IRA (The Bathroom). Contain the mess. Tax-Efficient Assets (Growth Stocks): Put them in the Brokerage Account (the Living Room). Let them shine. This simple reorganization can save you thousands of dollars a year. It costs nothing. It is just good design.

The Harvesting System

A smart house captures energy. A smart portfolio captures losses. When the market drops, we don’t cry. We “tax loss harvest.” We sell the loser to bank the tax deduction, then immediately buy a similar asset to stay in the market. We turn the lemon into lemonade. We use the government’s rules to lower our bill. You can build the perfect house. But if you never clean the gutters, the roof will rot. The final piece of the architecture is You. Behavior is the maintenance crew.

The Rebalancing Act

Every year, the house settles. The allocation drifts. If stocks go up, your roof gets too steep. You are taking too much risk. You have to trim. Definitely you sell the winner (high) and buy the loser (low). This is painful. It feels wrong. You want to let the winner ride. But responsible architecture requires discipline. You must rebalance to keep the structure sound.

The Emotional Thermostat

When the market crashes, the temperature drops. The emotional thermostat kicks in. Most people panic. They turn up the heat (sell everything). They blow up the furnace. A strategist sets the thermostat and locks the cover. When we know winter is coming. We don’t act surprised when it snows. We just put on a

sweater and wait.

The Final Inspection

Look at your financial life right now. Be honest. Do you have a roof (crypto/stocks) but no foundation (cash)? Do you have walls (insurance), or are you exposed? Is your plumbing (taxes) leaking money everywhere? Wealth is not a product you buy. This is a structure you build. It takes time. It takes blueprints. And it takes the discipline to pour the concrete before you pick out the curtains.

Stop trying to get rich quick. Start trying to build strong. Because when the storm comes—and it will—the only thing that matters is the architecture.

Disclaimer:

Look, Admin has been doing this a long time, but I’m a strategist, not your specific financial advisor or lawyer. The markets and regulations mentioned here, like the FinCEN rules or tariff situations, change faster than the weather. This article is meant to make you think strategically, not to replace professional advice tailored to your exact situation. Always do your own due diligence and consult with qualified professionals before making major moves.